Insurance: a move to the new direct-to-consumer (D2C) model in Asia

Although insurance purchasing practices vary significantly between countries in Asia, they are all shifting to online sales.

New 100%-digital businesses such as ZhongAn have won major market share from traditional insurers, which are becoming increasingly dependent on online distribution platforms. This is why Asian insurers are focusing their strategy on the direct-to-consumer (D2C) model. Its advantages: being able to offer customers a personalised digital service by collecting as much data as possible directly, and without having to pay commission.

100%-digital businesses that set the tone

Zhong An, the first 100%-digital Chinese insurer

Screenshot of the ZhongAn interface with insurance categories, profile and access to recommendations.

ZhongAn, initially the result of a collaboration between Alibaba, Tencent and the insurer Pen An, got into the insurance market in 2013 selling micro-insurance policies on third-party partner platforms (e-Commerce, transport, etc.). With 330 partners, ZhongAn is now implementing a diversification strategy to avoid being overly dependent on them. Since 2015, ZhongAn has reduced the number of intermediary sales in favour of D2C sales. To do so, the digital insurer is banking on technology and customer experience. It uses artificial intelligence to automate 70% of its online customer service and in 2018 launched its ZhongAn ANswer chatbot, which enables it to recommend insurance with 94% accuracy.

Customer service integrates technology at different levels: online sales uses targeted marketing, AI fights against fraud, policies are managed using Blockchain, and sign-up and refunds rely on visual recognition. As a consequence of this excellent customer experience, young customers (56% aged under 35 years old in 2018 according to ZhongAn), who want to sign up for their first insurance policy with ZhongAn, choose to remain loyal and directly sign up for new contracts every year.

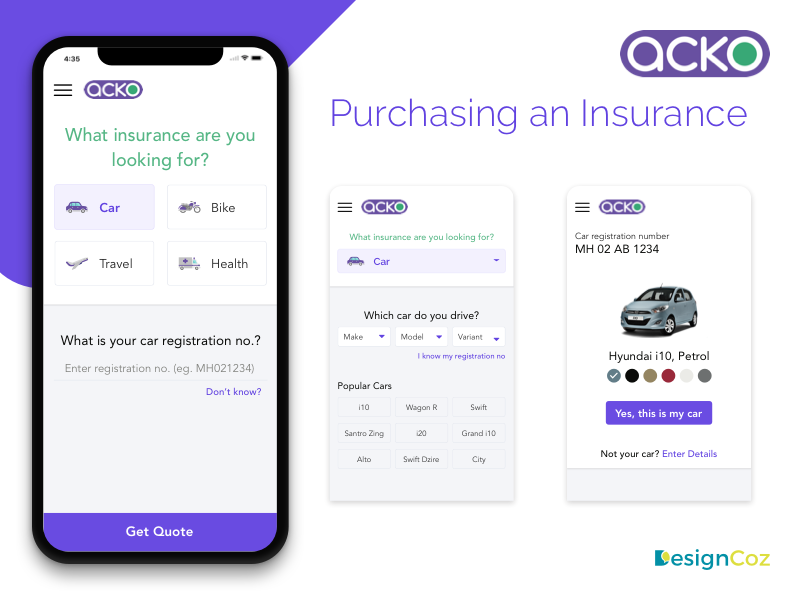

Acko General Insurance, the firm shaking up motor vehicle insurance in India

In India, Acko General Insurance saw exceptional growth as it digitally marketed motor vehicle insurance products. After its launch in 2016, the start-up actually provided coverage for 20 million customer the same year(1)!

Application interface - Source Acko General Insurance

Its 100%-digital strategy enables it to reduce its acquisition and sale costs, making it more competitive than traditional insurance firms. With more than 50% direct sales, it is capable of collecting data (type of car, region, history) to improve its customer service and provide custom pricing(2).

Insurers’ dependency on third-party platforms

A certain number of platforms and new intermediaries have emerged over the last decade, on which insurers have become increasingly dependent. These include online comparison platforms and platforms integrated into super apps or social networks. For example, 66.2% of non-motor vehicle insurance in China was marketed on third-party platforms in 2019(3).

This is why the Chinese tech giant Tencent launched the WeSure platform in 2017, giving customers the chance to purchase insurance products and receive refunds directly via QQ social apps and Tencent’s super app, WeChat. WeSure focuses on UX and partners with firms like Taikang for their insurance expertise. The platform now has 20 partner insurers and 55 million customers, and has already insured 25 million users(4).

WeSure is accessible via the QQ and WeChat applications. Source: adn-co

WeSure collects customer behavioural data, which enables it to make recommendations to its partners on the design of new insurance solutions. New services have been designed, such as for example the WeFit service, which encourages users to adopt a healthier lifestyle through sports competitions with friends or family. The more active the user is, the more reductions they get on their insurance, medical check-ups, gym membership, and even sports equipment purchases.

PolicyPal application interface - Source: ladyboss.asia/

Another example of a platform that has successfully set up shop in Asia is PolicyPal. This Singaporean firm positions itself as an “insurance guide” enabling users to better manage their insurance policies by scanning their paper documents, centralising them, and analysing their data using visual recognition (identification of zones not covered to advise on purchasing additional insurance).

PayTm super app services - Source PayTm.com

In India, PayTm is an example of a fast–growing super app. It is 42%-owned by… Alibaba. Originally designed as a payment wallet, the application has already proved a phenomenal success after India adopted its demonetisation policy (in November 2016, the government suddenly announced the withdrawal of 500 and 1,000 rupee notes from circulation to curb corruption5). The measure gave a real boost to PayTm: its user numbers doubled the following year. PayTM developed numerous additional services such as bill payment, and purchasing of bus passes, cinema tickets, and insurance. Following the award of its intermediary license in March 20206, the start-up is set to market products from 20 Asian insurers (life, health, motor) on its platform.

Traditional firms take the direct-to-consumer route

Chinese insurance firms have a head-start in the field of direct sales. In 2019, 45.8% of motor vehicle insurance policies in China were marketed directly on the firms’ respective applications. 22.5% of sales were then made on the WeChat accounts of these same firms. Today, all Chinese insurers have their own online distribution service. One of the pioneers is Ping An. All services, from sign-up to refund requests, can now be provided online: users enter their information, receive a quote, pay their fees, receive their policy by e-mail, then a certificate in under 2 days. They can then submit quick compensation claims on the application and receive their benefits within 3 days.

Screenshot of the Ping An app’s home page, after sign-up.

In addition to the chatbot answering questions, PingAn uses AI to assess benefit claims. Its strategy is to set up an all-in-one motor vehicle insurance service. The application can be used to find a parking space, request breakdown assistance, sign up for or renew an insurance policy, assess the damage caused in case of an accident, or contact customer service.

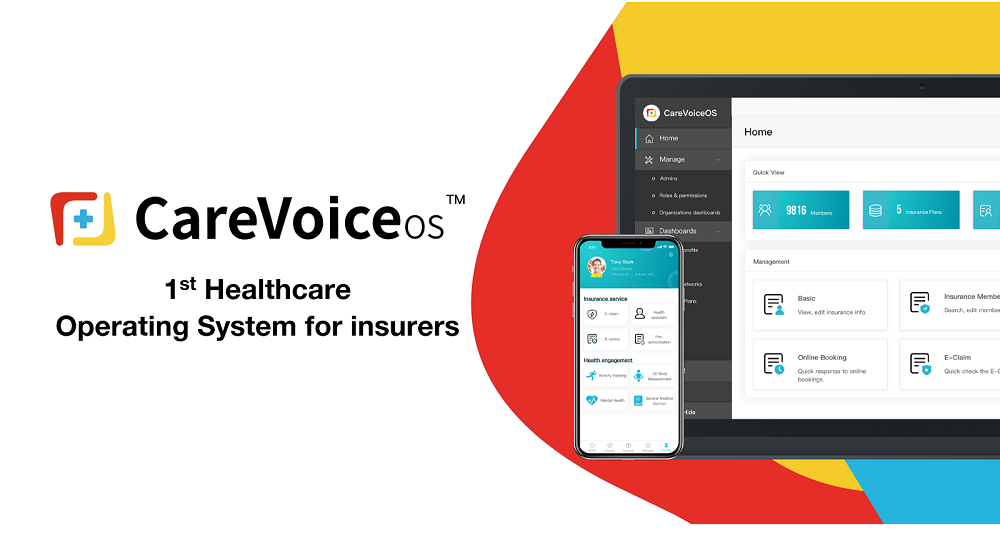

Screenshot of The CareVoice, the e-insurance Saas - Source: The CareVoice.com

Another element of this ecosystem is the start-up The CareVoice. It proposes an SaaS B2B platform, launched in 2019, to help traditional firms offer direct, online services. The CareVoice already collaborates with 15 insurance firms including Ping An, ZhongAn, P&C Insurance, and AXA. The aim is to bring insurers as close as possible to their customers via a digitalised and ultra-customised medical service (consultation, health monitoring, making appointments) and a digitalised insurance service (claims, virtual assistant, possibility of discovering and purchasing new insurance policies according to user needs).

Asia is once again a pioneer in digital transformation. Over the last few years, Asian insurers have seen the arrival on the market of new firms and intermediaries, which have forced them to accelerate their transformation and digitalise their services. Direct sales (D2C) enable them to set lower, personalised prices, and require them to constantly innovate to improve online customer experience. Customers then have access to faster, more transparent and effective purchase and refund services, as well as advisory services available at any time online via chatbots and robo-advisors.